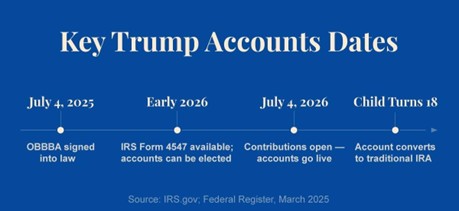

A new federally created savings account for American children will launch on July 4, 2026, when Trump Accounts will begin accepting contributions. These accounts were formally established under Section 530A of the Internal Revenue Code as part of the One Big Beautiful Bill Act.

Whether you have a newborn, a teenager, or grandchildren across multiple ages – we thought it might be helpful to give you an overview of what the accounts actually do, what they do not do, and how to think about them alongside what you may already have in place for the children in your life. This new account type has certain limitations and decisions that will depend on your family’s situation and goals.

What Are Trump Accounts, Exactly?

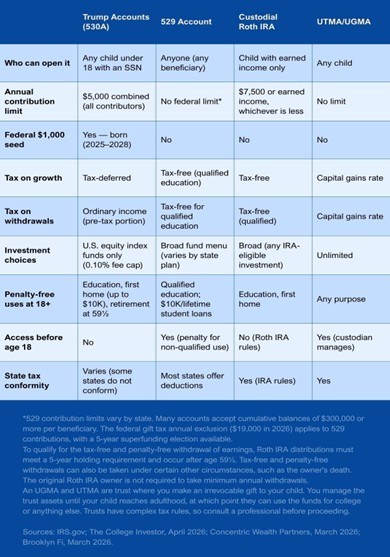

Trump Accounts were created for any child under 18 who has a valid Social Security Number and U.S. citizenship. The account is held in the child’s name, with a parent or guardian serving as custodian until the child turns 18, at which point the account is treated like a traditional IRA under standard IRS rules.1

For U.S. citizens born between January 1, 2025, and December 31, 2028, the federal government will make a one-time $1,000 contribution, called the pilot program payment — into children’s Trump Accounts to help kick-start their savings.1

Who Receives the $1,000 Federal Seed — and Who Does Not

The seed money is a detail that may be confusing, so it is worth stating clearly.

Children born between January 1, 2025, and December 31, 2028, who are U.S. citizens, may be eligible for Trump Accounts—and a one-time $1,000 federal pilot contribution deposited directly by the U.S. Treasury.

There are no income requirements to receive this contribution, meaning it is available regardless of family income. The election is made on IRS Form 4547.

By completing this form you’ll be modifying your tax return, and you are encouraged to consult your tax, legal, or accounting professional if you want to move ahead with a Trump Account.

Children born before January 1, 2025, do not receive the federal $1,000 seed. However, they may still open a Trump Account with all other features intact, provided they are under age 18 and have a valid Social Security Number. For families with older children, the account may still make sense as a supplemental vehicle, even without the seed contribution.

What Other Entities Are Making Contributions

The Treasury has announced that dozens of companies are prepared to match their employee contributions to their children’s accounts in various ways. Some companies have stepped up and said they are going to contribute to the accounts, and some others have said they will make contributions as part of their philanthropic initiatives. Taken together, these additional contributions may start to add up.2,3

This contribution is separate from the federal program and has its own eligibility process. Families in qualifying areas should monitor updates from the Invest America Council for details as they are finalized.

How Account Contributions Work

Once a Trump Account is open, here is who can contribute and how:4

- Parents, family members, friends, and the child themselves may contribute up to $5,000 per year, combined. This limit will be indexed for inflation starting in 2027.

- Employers may contribute up to $2,500 per year to an employee’s account or the account of the employee’s dependent. Employer contributions count toward the $5,000 annual limit.

- Governmental entities, state programs, and eligible 501(c)(3) charitable organizations may make qualified general contributions to a class of beneficiaries, such as all children born in a given year within a state or county. These contributions do not count against the $5,000 individual limit.

- There is no earned income requirement for the child. Contributions are after-tax (not deductible) for individual contributors.

One important tax distinction: Individual contributions from parents, family, and the child are made with after-tax dollars and are generally not taxable upon withdrawal. The federal seed, employer contributions, and charitable program contributions are treated as pre-tax and will be taxable as ordinary income when withdrawn.

This article goes over high-level information. Your tax professional can speak to your unique tax situation.

Where the Money Can Be Invested

There are constraints on where the assets in Trump Accounts can be invested. Account funds must be invested in low-cost U.S. equity index funds or exchange-traded funds. The law imposes a fee cap of 0.10% (10 basis points) annually.5

What that means in practice: Funds are concentrated in U.S. stock market exposure, without access to international equity, fixed income, real assets, or other asset categories. For an 18-year time horizon, a U.S. equity index allocation has historically performed well. The potential lack of asset class diversification and the presence of more conservative options within the account are factors families and their financial professionals should consider in the broader picture.

Exchange-traded funds are sold only by prospectus, which will provide more detail on the risks, expenses, and investment objectives. We encourage you to read the prospectus carefully. Asset allocation and diversification are approaches to help manage investment risk. Asset allocation does not guarantee against investment loss.

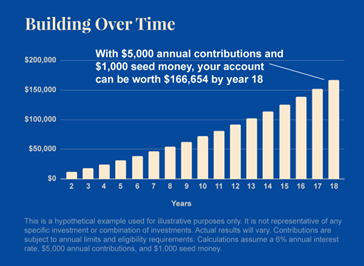

How Much Could Your Child’s Account Be Worth Before They Graduate High School?

What is the “Growth Period” of an Account?

The “growth period” for the beneficiary of a 530A account begins when the initial Trump Accounts were established and ends on December 31 of the calendar year in which the account beneficiary attains age 17. Generally, distributions from Trump Accounts are not allowed during the growth period.5

What Happens When the Child Turns 18?

At the end of the calendar year in which the child turns 17, the growth period officially closes. From that point forward, the account operates as a traditional IRA under standard IRS rules, and the child takes full ownership.

Penalty-free uses after age 18 follow traditional IRA exception rules, which include:

- Qualified higher education expenses (tuition, fees, required books, room, and board)

- First-time home purchase, up to $10,000 lifetime

- Withdrawals after reaching age 59½ for retirement

- Other traditional IRA exceptions under IRS rules (disability, certain medical expenses, etc.)

Once you reach age 73, you must begin taking the required minimum distributions from a traditional IRA in most circumstances. Withdrawals from traditional IRAs are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty.

There is also no requirement to use the funds for a specific purpose—the child may withdraw for any reason upon turning 18, though taxes and potential penalties would apply.

This last point is worth flagging in family conversations. Unlike a 529 account, which is structured specifically around education spending, Trump Accounts do not legally restrict the beneficiary’s access once they reach 18. Parents and grandparents contributing with specific goals in mind should factor this into their overall strategy.6

A 529 plan is a tax-advantaged education savings plan. Before choosing a plan, it’s important to consider not only the state tax treatment – but also any associated fees and expenses.6

How Trump Accounts Compare to Other Savings Vehicles

While Trump Accounts are a new tool, they are not meant to replace existing ones. How they stack up depends on what your family is trying to accomplish.

If education funding is your primary goal, you might want to consider a 529 account because of its tax-free growth and tax-free withdrawals for qualifying education expenses. If the goal is to focus on the future with flexibility beyond college, then Trump Accounts may play a role.

State Tax Conformity: An Important Variable

Federal tax treatment is only part of the picture. States are not required to conform to federal tax rules, and some do not. California, for example, does not currently conform to Section 530A. Families in non-conforming states may face state income tax on deferred federal growth. This is an area where guidance is still evolving and where involving a tax professional can help.

What to Do Right Now

The most time-sensitive action for families with children born in 2025 or 2026 is establishing the account and making the pilot program election to pursue the federal $1,000 contribution. Here is a checklist to consider:5

- If your child was born in 2025: File IRS Form 4547 through Trumpaccounts.gov.

- Contributions can begin after July 4, 2026.

- If your child was born in 2026 or later through 2028, file Form 4547 at any time before December 31 of the year the child turns 17.

- If your child was born before 2025 and is under 18, an account can still be opened without the federal seed.

- Regardless of birth year: Confirm your state’s tax conformity with Section 530A before making substantial contributions.

- Revisit your existing strategy: If you already have a 529 account, the Trump Accounts may work alongside it.

A Few Cautions

New account types take time for implementation guidance to settle fully. As of July 2026, several aspects of Trump Accounts are confirmed in statute, but IRS regulations are still being finalized. Key areas of ongoing guidance include specific eligibility verification procedures for the federal seed, gift tax treatment for contributions (particularly for grandparents), and final confirmation of withdrawal rules and penalties as they interact with traditional IRA frameworks.

Good recordkeeping matters from the start. Track the source of every contribution separately, because personal after-tax contributions and government or employer pre-tax contributions are taxed differently on withdrawal. Mixing records may complicate your tax strategy down the road.

If you’re considering Trump Accounts, a financial professional may offer some insights. The rules are real, the benefits are real, and the decisions about how to incorporate Trump Accounts into a broader savings strategy are genuinely individualized.

Frequently Asked Questions

Can Grandparents Contribute to Trump Accounts?

Yes. A parent, guardian, grandparent, or adult sibling can make an election for an eligible child and file Form 4547 on their behalf. Grandparents can also contribute to the account once it is open, subject to the $5,000 annual combined limit that applies across all contributors. The accounts are well-suited to multigenerational giving, but coordinating contribution amounts across family members matters.8

What Happens to Trump Accounts if My Child Does Not Go to College?

The account does not require an educational purpose. After the child turns 18, the account behaves like a traditional IRA, and penalty-free withdrawals are available for qualified higher education expenses, a first-time home purchase up to $10,000, or retirement after reaching age 59½. For any other use before 59½, withdrawals are subject to ordinary income tax plus a 10% early withdrawal penalty on the taxable portion.9

Can My Child Have Both Trump Accounts and a 529 Account?

Yes. There is no rule preventing a family from maintaining both Trump Accounts and a 529 account simultaneously. The two accounts might serve different purposes: A 529 account for education spending with tax-free qualified withdrawals, while Trump Accounts can be used for other things. 10

Should I Open a Trump Account Even if I Already Maxed Out a 529 Account?

It depends on your goals and tax situation, but the $1,000 federal seed for children born 2025 through 2028 is a straightforward reason to establish the account. If your child is eligible for the federal $1,000 contribution, filing Form 4547 online takes little time and costs nothing.7

Is There a Deadline to Claim the $1,000 Federal Contribution?

The last day to make a pilot program election for an eligible child is December 31 of the calendar year in which the child reaches age 17.5

For children born in 2025, the election can be made with the 2025 tax return or through TrumpAccounts.gov, and the earlier the account is established, the longer the $1,000 has the opportunity to grow before the child turns 18.

Interested in setting up a time to talk about financial planning for your family? Contact First Financial’s Investment & Retirement Center

Securities and advisory services are offered through LPL Financial (LPL), a registered investment advisor and broker/dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. First Financial Federal Credit Union (FFFCU) and First Financial Investment & Retirement Center are not registered as a broker/dealer or investment advisor. Registered representatives of LPL offer products and services using First Financial Investment & Retirement Center, and may also be employees of FFFCU. These products and services are being offered through LPL or its affiliates, which are separate entities from and not affiliates of FFFCU or First Financial Investment & Retirement Center.

Securities and insurance offered through LPL or its affiliates are:

This content is for informational and educational purposes only and does not constitute tax, legal, or investment advice. Trump Accounts rules are subject to ongoing IRS guidance. Consult a qualified tax advisor or financial professional before making decisions based on this content. Projected growth figures are hypothetical and illustrative only; past performance of any index does not guarantee future results. Copyright FMG Suite.

A 529 plan is a tax-advantaged education savings plan. Before choosing a plan, it’s important to consider not only the state tax treatment but also any associated fees and expenses. Availability of a state tax deduction will depend on your state of residence, as state tax laws and treatment may vary from federal tax laws. If you make nonqualified distributions, earnings will be subject to income tax and a 10% federal penalty tax.

Sources:

1. Investor.gov, April 2026

2. BusinessWire.com, January 29, 2026

3. APNews.com, December 2, 2025

4. IRS.gov, December 2, 2025

5. GovInfo.gov, March 9, 2026

6. PKFOD.com, April 2026

7. BrooklynFI.com, February 20, 2026

8. MilestoneFinancialPlanning.com, March 26, 2026

9. Knowledge.DLAPiper.com, March 30, 2026

10. ConcentricWealthPartners.com, March 6, 2026